{kind=link}

Did I say mandatory? I meant optional! You’re “free” to die in a cardboard box under a freeway as a market capitalist scarecrow warning to the other ants so they keep showing up to make us more!

Did I say mandatory? I meant optional! You’re “free” to die in a cardboard box under a freeway as a market capitalist scarecrow warning to the other ants so they keep showing up to make us more!

I don’t agree with unrealized gains taxes in general, but the instant they are used as collateral, or if value in any way is extracted from them (even loan value), they become realized gains, and should be taxed.

deleted by creator

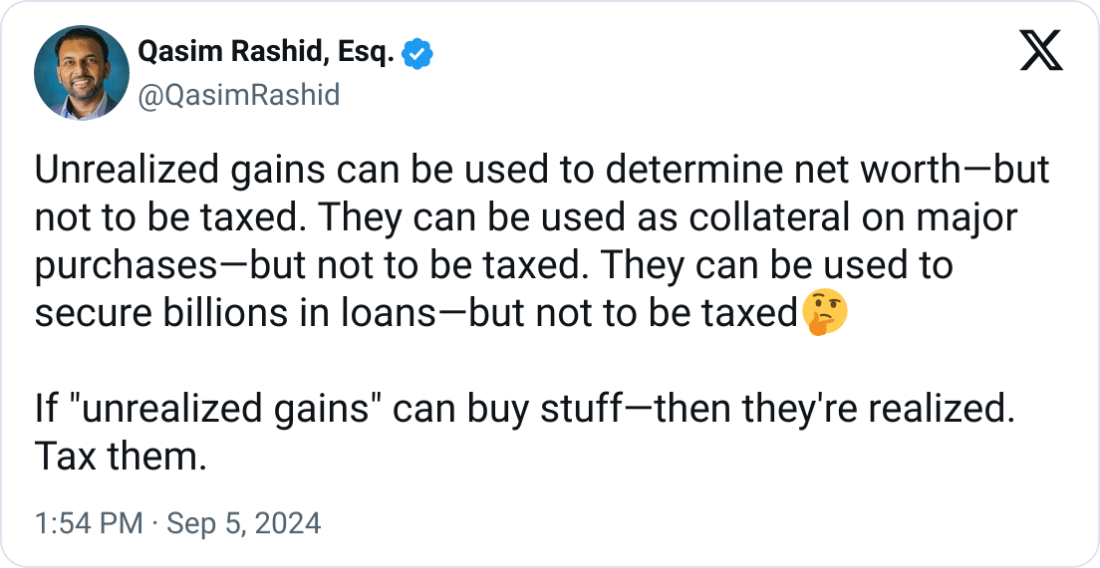

I think the key point in the post was “If ‘unrealized gains’ can buy stuff-then they’re realized. Tax them.”

Essentially, because the unrealized gains held in their stocks could be realized through a loan, all of their capital gains should be considered for taxation.

As opposed to just the assets used as collateral, that is now effectively liquid, should be taxed as realized.

I personally think we should do everything we can to disincentivize wealth hoarding, even if it’s an “unfair” or possibly somewhat broken system that does so, but it also doesn’t seem feasible as a kind of legislation you could convince anyone in the government to enact, since they’ll still be focusing on things like if it could possibly lead to a higher loss than the initial investment if they’re taxed on the gains for years, but it drops low enough to wipe out all the value they paid in tax and their gains, even if the actual price is higher than the purchase price.

Yeah, a bank isn’t going to give your a $500k mortgage on a $200k property, so if they give you a $500k loan on stock then that’s the value given to the stock at that point.

What you’re suggesting would also mean you’re advocating for middle class homeowners to be taxed on a full value of a Home Equity Line of Credit (HELOC) even if they haven’t spent a dime of it yet. Was that your intention?

Homeowners are excluded from capital gains tax for the first 250k for individual filers.

I believe you’re referring to rules on sale of a home where there is a capital gain, meaning you bought the house for $100k and sell it for $350k, no cap gains taxes. We’re in uncharted waters with what @[email protected] is proposing. That user (possibly) suggesting it for HELOCs too.

Okay but you can just apply the same logic to a HELOC. If you get a 30k HELOC for a bedroom renovation then it does not count towards capital gains tax.

Even normal capital gains taxes have brackets.

Wouldn’t this be a double standard if we’re applying @[email protected] 's logic? The rich would get taxed on loaned money but the middle class wouldn’t?

That’s generally how progressive tax brackets work, yes. Technically speaking if I rich person wants to take out a 30k HELOC they’d also not get taxed on it.

that’s like the point of the entire system? I mean, I don’t want to go back to the 1800s corporate baronies that defined most industry at that point in time

This is how… EVERYTHING works… Income tax brackets, 401k limits. I thought this was pretty obvious, from each according their ability and all.

Oh no… Anyway.

Oh no, I guess our legislators’ hands are tied. It’s not like they could just put an exemption for a person’s first home into the law or anything.

Oh well.

deleted by creator

They didn’t set out their whole tax platform for their presidential bid friend. We can trivially blow down your straw man with a primary residence exemption or, you know, tax brackets.

Simply tax it as if it underwent a buy/sell/trade. Capital gains and losses are accounted for in that at the time the value is utilized. They are tracked, and you don’t pay them later.

Reasonable home ownership (only home) could be exempted.

How does this actually make any sense though? All collateral is, is a safety net to mitigate loss for a lender who lends to someone who then defaults on the loan. If the loan is not defaulted on, literally nothing happens to the collateral.

How then does it make any sense to consider the mere act of the loan being given as a realization of the collateral, in other words, equivalent to having sold the collateral, when literally nothing has happened to it?

This feels completely arbitrary. Using an asset as collateral is nothing like realizing it.

And WHAT gain exactly is being taxed? So you have a $1000 investment. The government decides, what, that you are a good investor and can make 20% so they’ll tax you on $200? So if you sell it at a loss, you get screwed. If you sell it for a 50% gain the government loses tax revenue? You know what, I’ll take that deal. I’ll invest money, pay the taxes on my unknown gain immediately, keep it for 20 years and boom, tax free, because I’ve already paid the taxes on the gain. You know I’m totally on board with this whole rich people suck idea, but this is just stupid.

ok, so I understand that you don’t quite get the issue, also your bad at taxes.

if I invest $50000 and make $100000 I don’t want to pay taxes on the $50000 I “made” (this normally would lead to the crime of not paying taxes) but if I use those $50000 as leverage on an extremely low interest loan for $50000 then I dodge having to pay anything in taxes while also, defacto, realizing my gains.

what OP is advocating for is taxing those $50000 you put up as collateral, making these $50000 similar to the original $50000 you invested, now should you again make another $20000 from said capital, and pull out, you would still have to pay capital gains on those $20000, or do you think you have to pay capital gains on money you put in? (hence why you’re bad at taxes) because tax is only levied on the positive difference

I love the way people on the internet have to insult to make a point.

I’m just glad you’re not the one making the tax laws.

I’m not insulting anyone, if you feel slighted about the fact that you didn’t understand OP, nor do you understand how taxes work, then I invite you to do some basic research about tax law in the US, because you don’t seem to know how taxes work

You know, I heard that rich people need air to live, we should totally tax the crap out of that. That would show them.

you’re lacking English or economic comprehension skills are no reason to start creating straw men, you’re wasting all that bedding for the rest of your fellow sheep

Realization is the establishment of value not sale for cash (it just happens that the most convenient establishment of value for any non-fungible asset is sale). There are already some realization events that don’t have associated cash flows, to do with overseas assets or certain financial instruments. Ordinary people don’t need to worry about this stuff, it’s not for them, and if you’re rich you can trivially figure out the cash flow issue.

But capital gains avoiding tax for the life of a wealthy person who lives off collateral zed borrowing, then being stepped up in basis for their heirs is just embarrassing for the US.

Absolutely nonsensical massive straw-grasp. If that was true, that would mean that everything that HAS a widely-established market price is instantly and permanently to be considered realized by everyone who owns it.

Relevant case law: “While it is true that economic gain is not always taxable as income, it is settled that the realization of gain need not be in cash derived from the sale of an asset” https://supreme.justia.com/cases/federal/us/309/461/

It is in fact true, and clearly then doesn’t mean that at all. We can and do control what constitutes a realization event, and borrowing is a pretty sensible candidate. I don’t know why you’re losing you mind over this fairly prosaic idea.

You left out some pretty important context in that quote to make it seem like it’s saying that realization is arbitrarily decided. In truth, all this is saying is that realization is not confined to reception of cash itself:

As it says at the end there, the ways to realize gain all necessarily entail “profit”. A loan is not profit, nor is an already-owned asset transform into profit when used as collateral.

The above could absolutely not be used to support your argument, nor refute mine–not when you read it honestly and in context.

The capital gain is the profit, the collateralized lending is the transaction completed to realize that profit. It’s a logical extension of accepted understandings of those terms and easy to imagine coherent legislation to implement.

You don’t like the idea, that’s fine. But it’s simply not true to claim that it doesn’t make sense and you haven’t been able to articulate any inconsistency. Just saying “nuh uh that’s not profit” is pointless. We all know it doesn’t constitute realized gain in the existing system of laws, but OP and others are suggesting it would a be a sensible way to tax the extraordinary benefits that the ultra-wealthy take from their appreciated assets. It’s been explained to you politely and with sources, if you have nothing more serious to add to the conversation I’m done giving you the benefit of the doubt.

Wait…I pay taxes on my HELOC…